Vitec Software Q2 2026: the machine is running, the market is wrong to be afraid

The numbers speak, the fear doesn't hold up. Full breakdown of the quarter, the conference call, and what AI really changes for Vitec.

Vitec Software published its second quarter 2026 results this morning. The stock has lost more than half its value in a year (228 SEK vs. 477 SEK twelve months ago), driven by a diffuse fear: will AI destroy vertical software companies?

The numbers tell a different story. Here’s what you need to know.

Valuation: let’s talk about it honestly

Before diving into the results, a word about what matters most to any investor: the price you pay.

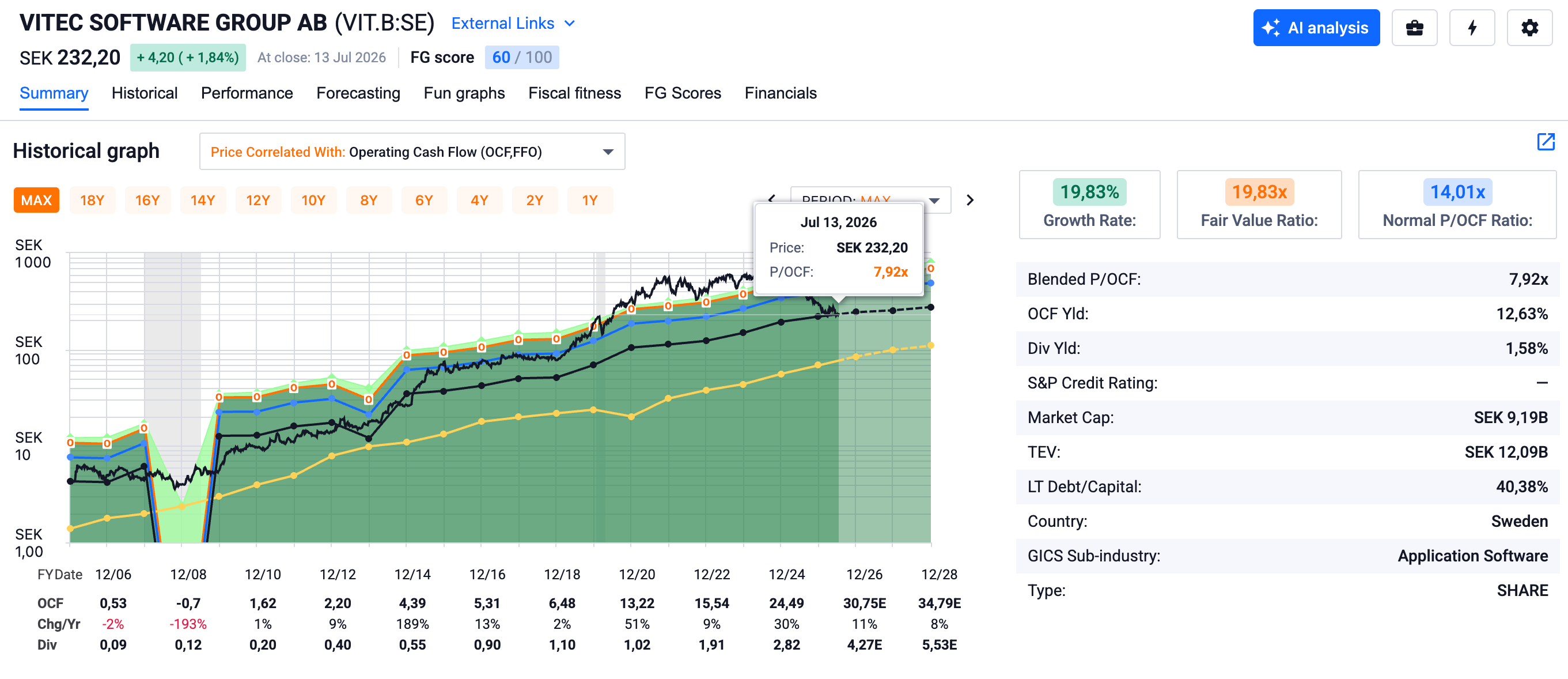

At the current price of 232 SEK, Vitec trades at a P/OCF (Price to Operating Cash Flow) of 7.92x. For a company with a historical growth rate of 19.8% per year, an OCF yield of 12.6%, and an estimated fair value ratio of 19.8x according to FastGraphs, the picture is straightforward: the stock is trading today at less than half its normal valuation.

The historical chart is striking. The price line has fallen well below the fair value zone, something that had virtually never happened over the past 20 years. The market is pricing Vitec as if growth were about to collapse. Yet this quarter’s fundamentals say exactly the opposite.

Operating cash flow per share went from 0.53 SEK in 2006 to an estimated 30.75 SEK in 2026. That’s a 58x multiplier in twenty years. The dividend followed the same trajectory, from 0.09 SEK to an estimated 4.27 SEK. This is a compounder of the finest kind, and it is trading today at a multiple not seen in years.

Does this mean you should rush in? No. But it means that the market is offering you a historically rare entry point on this quality of business model.

What’s going well, and it’s what matters most

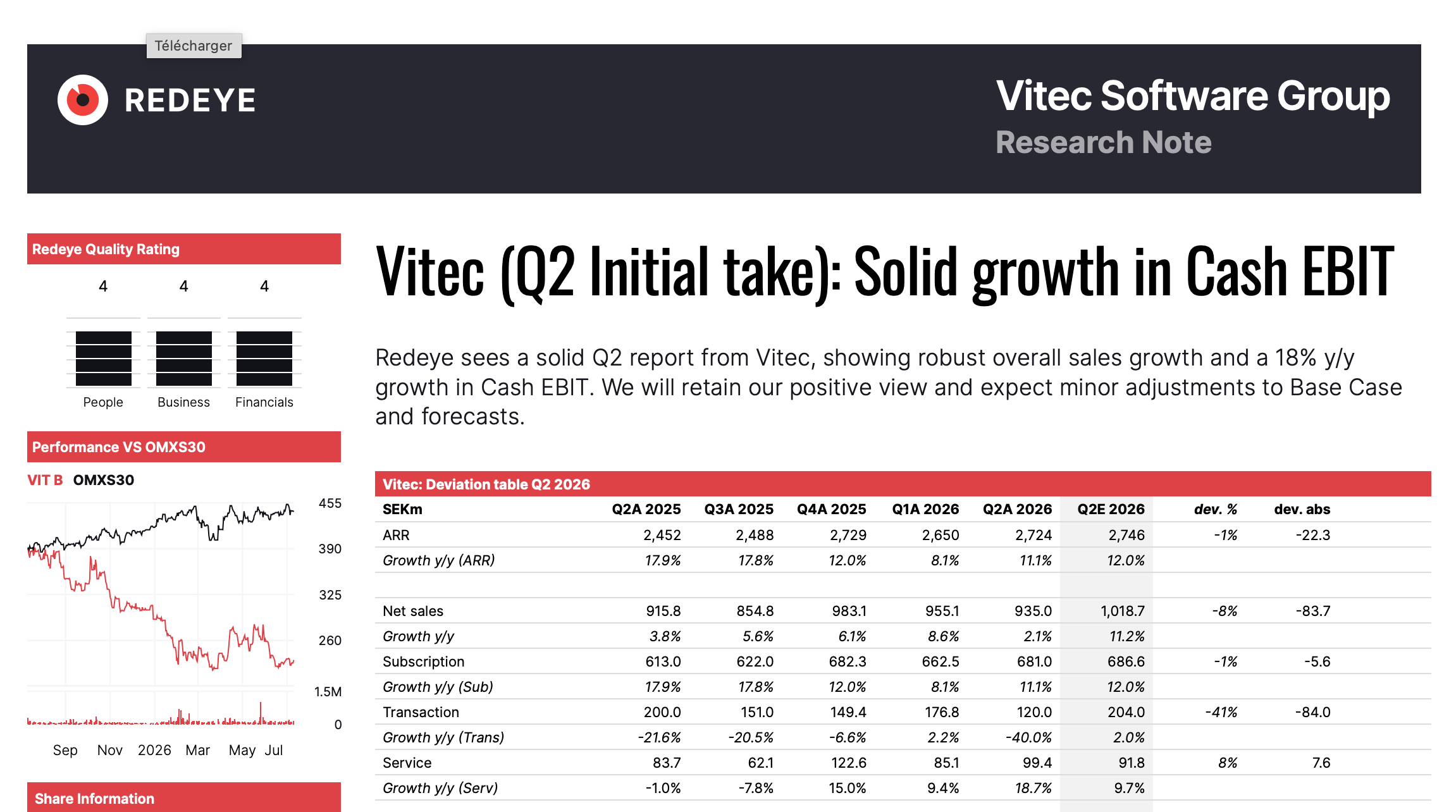

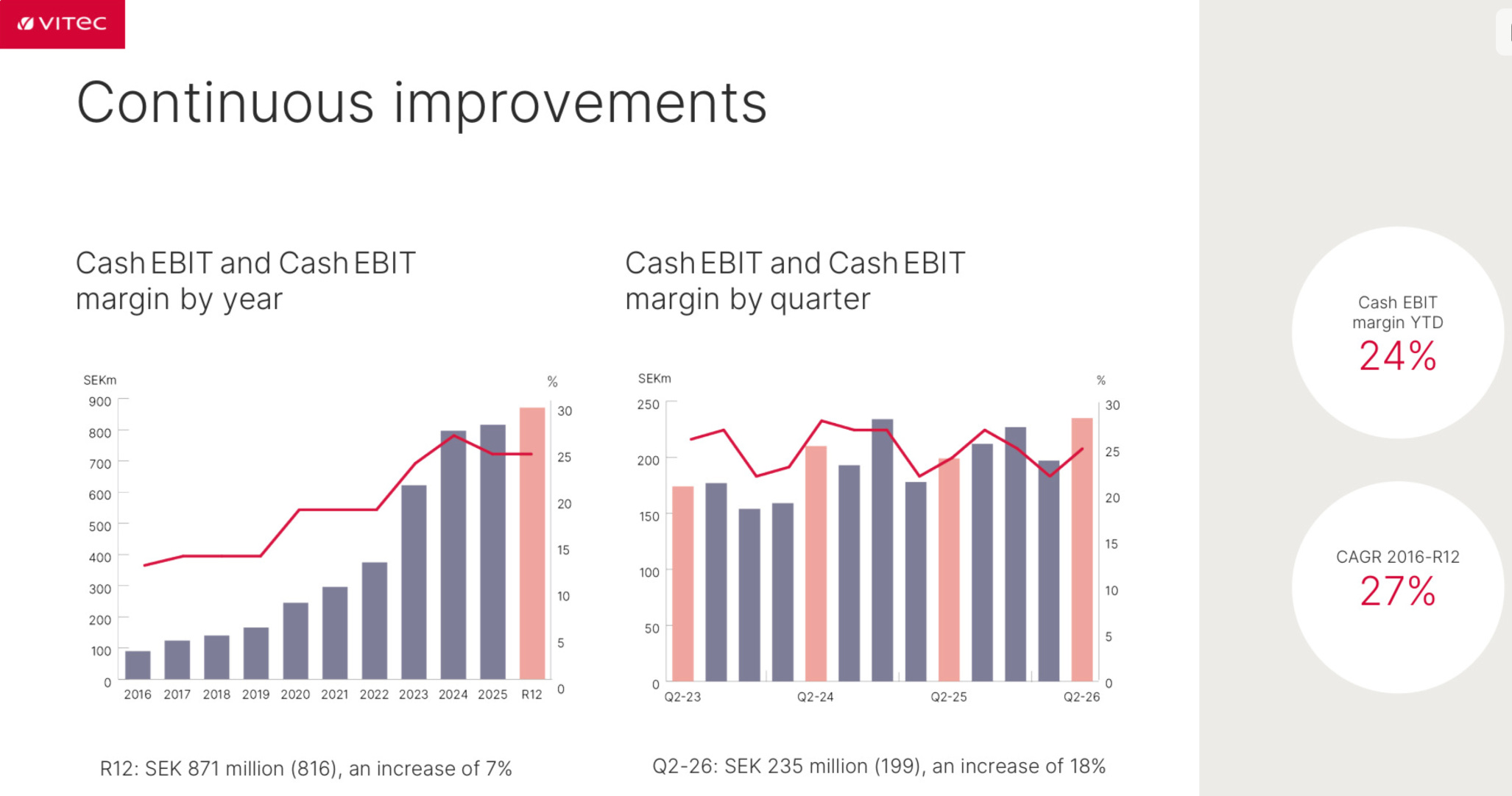

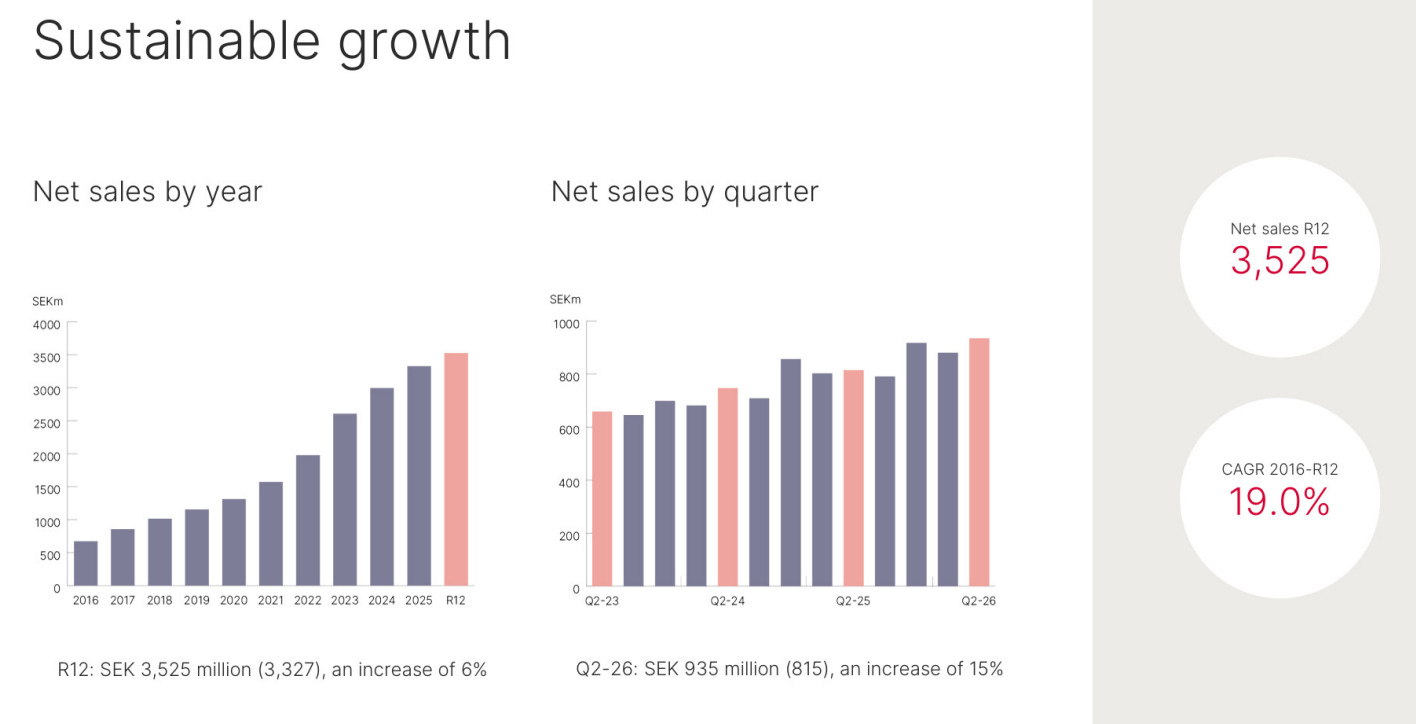

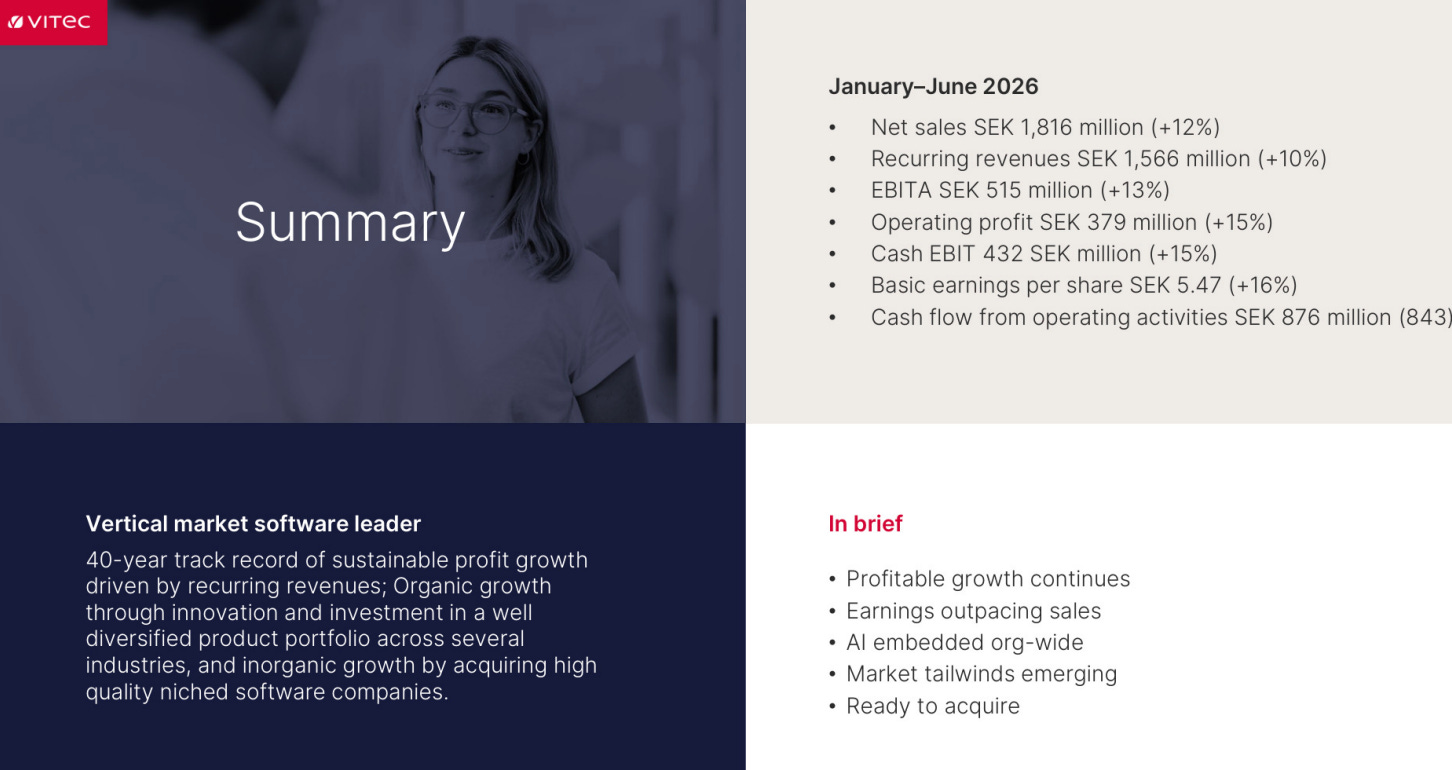

Revenue is up 15% to 935 MSEK, including 4% organic growth. The Cash EBIT margin, Vitec’s true cash profitability indicator, rises to 25%, one full percentage point higher than a year ago, with an 18% increase in absolute terms. CEO Olle Backman doesn’t mince words:

“It’s really one of our absolutely best quarters in terms of Cash EBIT performance.”

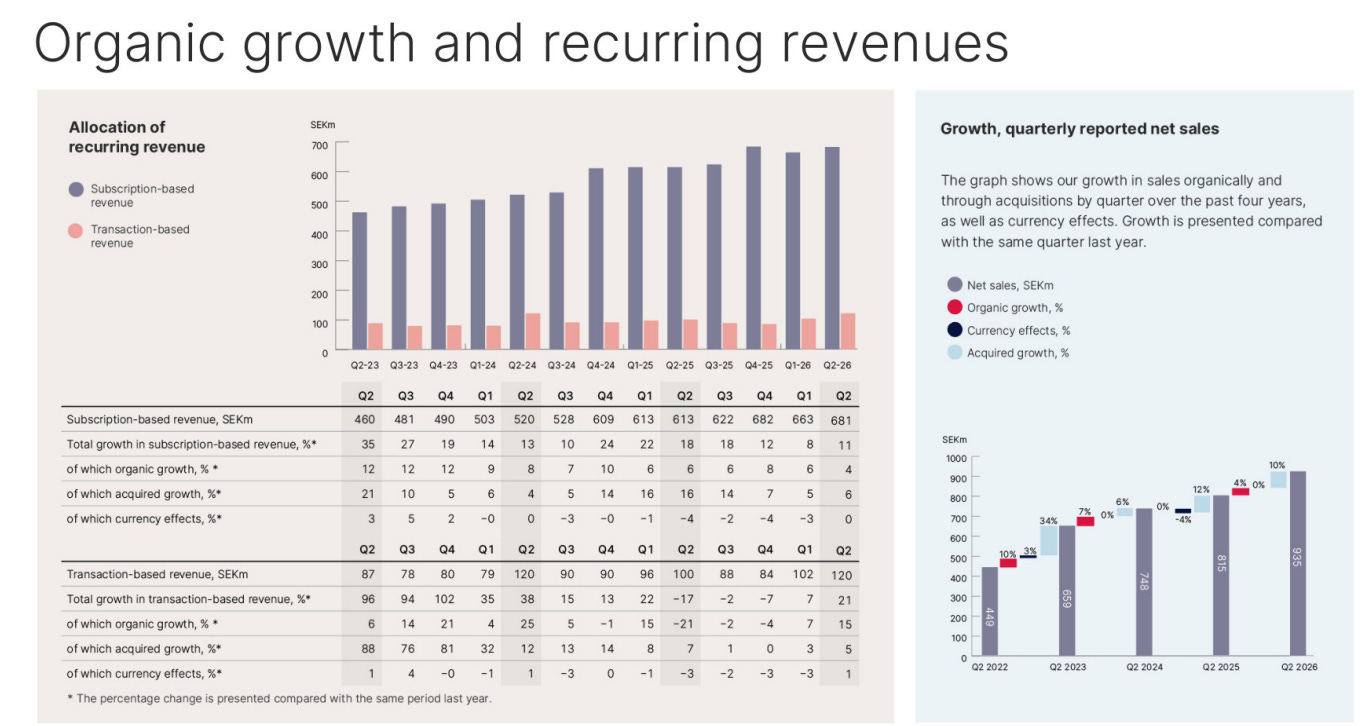

86% of revenue is recurring. Subscription revenue grew 11%, transaction-based revenue 21%. That last figure is particularly telling: it reflects a real pickup in customer activity, especially in Norwegian real estate where broker Vitec Megler posted over 30% transaction revenue growth.

Operating cash flow for the first half reaches 876 MSEK vs. 843 a year earlier. A quick reminder of how the Vitec model works: nearly all of the year’s cash flow is collected in Q1 thanks to upfront billing of subscriptions. The rest of the year is steady and predictable. This is a model that funds its own acquisitions.

Concrete signs of a recovery

This might be the most important takeaway from the quarter, and you won’t find it in the numbers. You’ll find it in the conference call. Olle Backman was unusually explicit about the improving business climate:

“When you contact a customer, you can get a meeting within a week or two rather than, okay, don’t call me. I will call you in three months’ time.”

Three sectors are driving this recovery: PropTech / property management, healthcare and welfare, and real estate agents (Sweden and Norway). The order book is filling up, sales cycles are shortening, pilots are multiplying.

But Backman warns: none of this will show up in revenue for several months, because the systems Vitec sells are complex and take time to implement.

“If we’re signing orders today, there is an implementation. That’s the beauty of it. We are delivering mission-critical, quite complex systems. It shouldn’t be easy either to just put them in or to take them out.”

It is precisely this complexity that protects Vitec. What takes a long time to sell also takes a long time to lose.

AI: what you need to understand once and for all

The market is treating Vitec as if ChatGPT were about to replace a Finnish power grid management ERP or a Danish pharmacy software. This is a fundamental misunderstanding of what Vitec does.

Backman was very clear on this during the call:

“We haven’t really seen any customer churn just on the basis of AI yet. You don’t rewrite an entire ERP system that easily, and for sure you don’t exchange it. These are very slow-moving things, and they should be. That’s why they are mission critical.”

The reality is the opposite. AI is becoming a growth lever for Vitec, not a threat. Several concrete examples were shared during the conference call:

Vitec Fastighet (property management in Sweden) has spent the past two years building an ecosystem of AI agents integrated into its software. The system is evolving from a simple “system of records” into an intelligent platform with automated customer support, text generation, and multilingual assistance.

Vitec Acute (healthcare in Finland) is automating clinical documentation through AI, while respecting the regulatory and security constraints specific to the hospital sector.

Vitec Tietomitta (waste management in Finland) has fast-tracked the development of a brand-new version of its software using internal AI tools.

Vitec Energy is using AI to improve the quality and diversity of energy forecasting models delivered to its clients.

The crucial point: customers are starting to ask for these features. Backman notes a shift in tone compared to the previous quarter, when customers were still cautious.

“For sure, there’s more interest, more openness, and willingness to try as well. They usually do pilots and things like that. We have lots of that ongoing at the moment.”

And most importantly, this added value can be monetized:

“If you can prove to your customer that by using this, for instance, some agentic function, their processes become more easy, they can save money on it. You have a possibility to have a dialogue around, okay, what is the customer value and what part of that should we be rewarded for?”

Check out my YouTube channel! (Switch to English audio in settings)

What deserves your vigilance

A good analyst doesn’t only look at what shines. Here are the points to watch.

Debt has risen sharply. Net interest-bearing debt goes from 2,105 MSEK to 3,013 MSEK in one year, a 43% increase. Add in acquisition earn-out commitments (627 MSEK) and you reach 3,639 MSEK in total adjusted debt. Vitec issued 700 MSEK in bonds in February and drew 1.3 billion from its credit facility during the half. Net financial expenses rose 20% to 63.5 MSEK for the semester. The equity-to-assets ratio dropped from 48% to 44%.

This is not alarming given the predictability of cash flow, but the trajectory is expansionary and deserves to be monitored quarter after quarter.

Organic growth remains modest. 4.4% on subscription recurring revenue in Q2. Backman was transparent during the call: roughly 2 to 2.5% comes from price increases (CPI-indexed, declining vs. last year) and the rest from new volumes. He expects pro forma organic recurring revenue growth of around 5 to 6% on a normalized basis, perhaps one point less as the inflationary tailwind fades.

“The pricing component will go down a bit. That leaves it at the number of roughly 5%-6%, where we have seen over the years that that has been a fairly normal number for us.”

The tax rate is structurally higher. 26% in both Q1 and Q2, above historical levels. The reason is simple and lasting: Vitec is generating more and more profits outside Sweden (Netherlands, Belgium, Poland, Finland), in jurisdictions with higher corporate tax rates. Backman confirmed that the current level is the right proxy going forward.

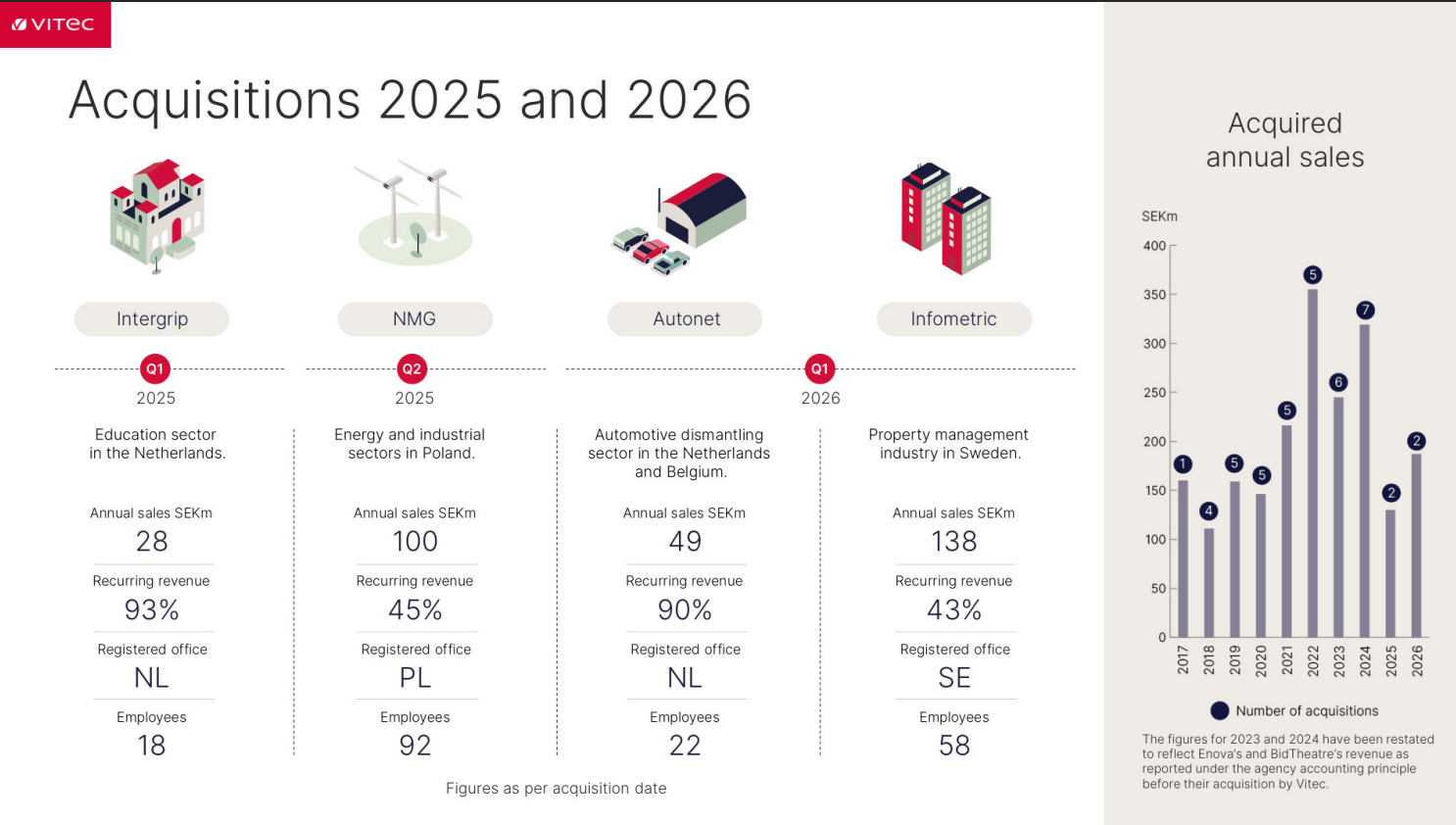

No acquisitions in Q2. Vitec signed nothing this quarter. Two deals were closed in Q1 (Autonet and Infometric, combining roughly 190 MSEK in revenue). The M&A pipeline is active, but Backman is emphatic about valuation discipline:

“We are really not driving the prices upwards anyway, we are still losing more than we’re winning because we really firmly believe that we will put a fair value on this asset.”

This is reassuring for long-term shareholders. Vitec does not overpay to grow.

The accounting change: what you need to remember

Starting this quarter, Vitec reports revenue from two subsidiaries (Enova and BidTheatre) on a net rather than gross basis (so-called “agent accounting”). In practice, Enova which previously showed roughly 300 MSEK in revenue now appears at roughly 100 MSEK, and BidTheatre goes from roughly 150 MSEK to roughly 36 MSEK.

Net income, cash flow, EPS and financial position are completely unchanged. Only reported revenue drops by approximately 8% and margins mechanically rise by 2 percentage points. All historical figures have been restated going back to Q1 2023 to ensure comparability.

This is a technical adjustment in line with ESMA guidelines, intellectually more honest, but it complicates comparisons with older reports or articles.

My overall take

Vitec delivered a solid quarter, fully in line with its model. The company is doing exactly what you own it for: generating recurring cash, acquiring with discipline, gently pushing prices higher in captive niches, and starting to turn AI into an organic growth lever rather than a threat.

The market is currently pricing a disruption scenario that does not match the operational reality of 49 business units deeply embedded in their customers’ workflows. When your software manages the clinical documentation of a Finnish hospital or the energy balance of a district heating network, nobody replaces you with a prompt.

At 7.9x operating cash flow, versus a historical average of nearly 20x, the market is offering you an entry point that long-term shareholders have almost never seen. This guarantees nothing in the short term. But for those who understand this business model and are willing to be patient, the risk-reward is currently tilted in the buyer’s favor.

The real risks lie elsewhere: rising debt, structurally single-digit organic growth, and an acquisition market that could become more expensive if AI makes small vertical software companies more profitable and therefore pricier.

But for a patient shareholder, the fundamentals of this quarter are reassuring.

As always, this is not investment advice. Do your own research, read the full report, and never make a decision based on a single source.

As always, this is not investment advice. Do your own research, read the full report, and never make a decision based on a single source.